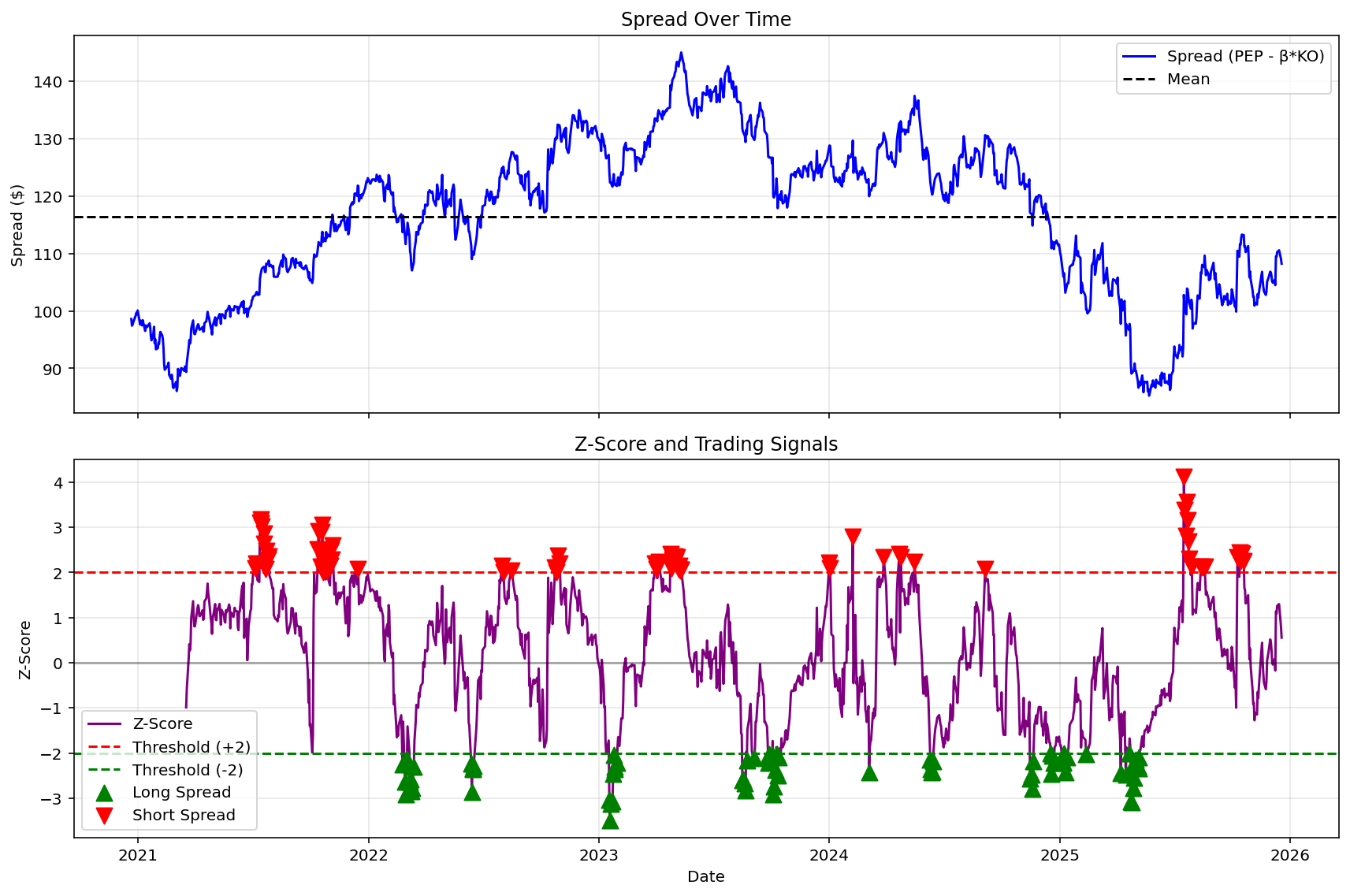

The Hedge Ratio Should Never Be Static

Why a static hedge ratio breaks pairs trading strategies, and how to implement a rolling OLS regression in Python to …

Read more →Systematic options trading, Python code, seasonal patterns, and the data behind every decision.

Why a static hedge ratio breaks pairs trading strategies, and how to implement a rolling OLS regression in Python to …

Read more →

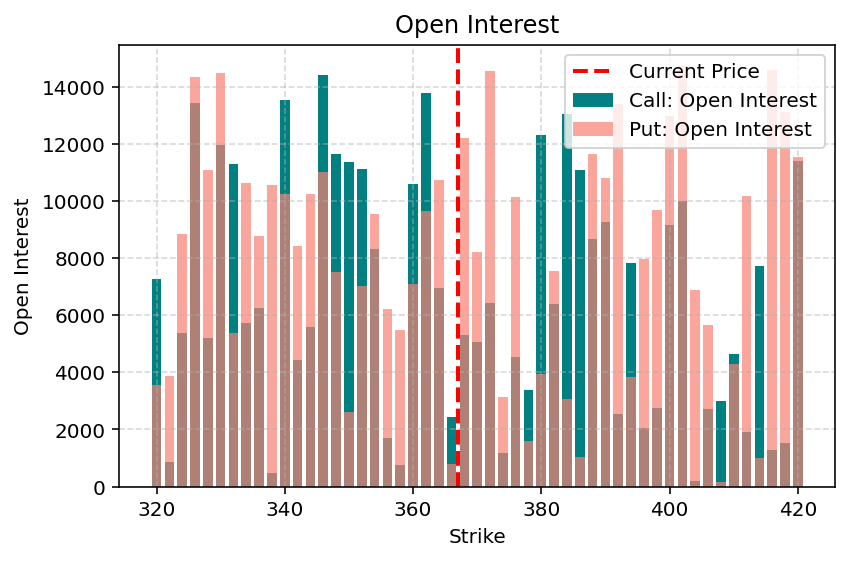

How to read and interpret options volume and open interest in Python, what they mean, why they matter for execution, and …

Read more →

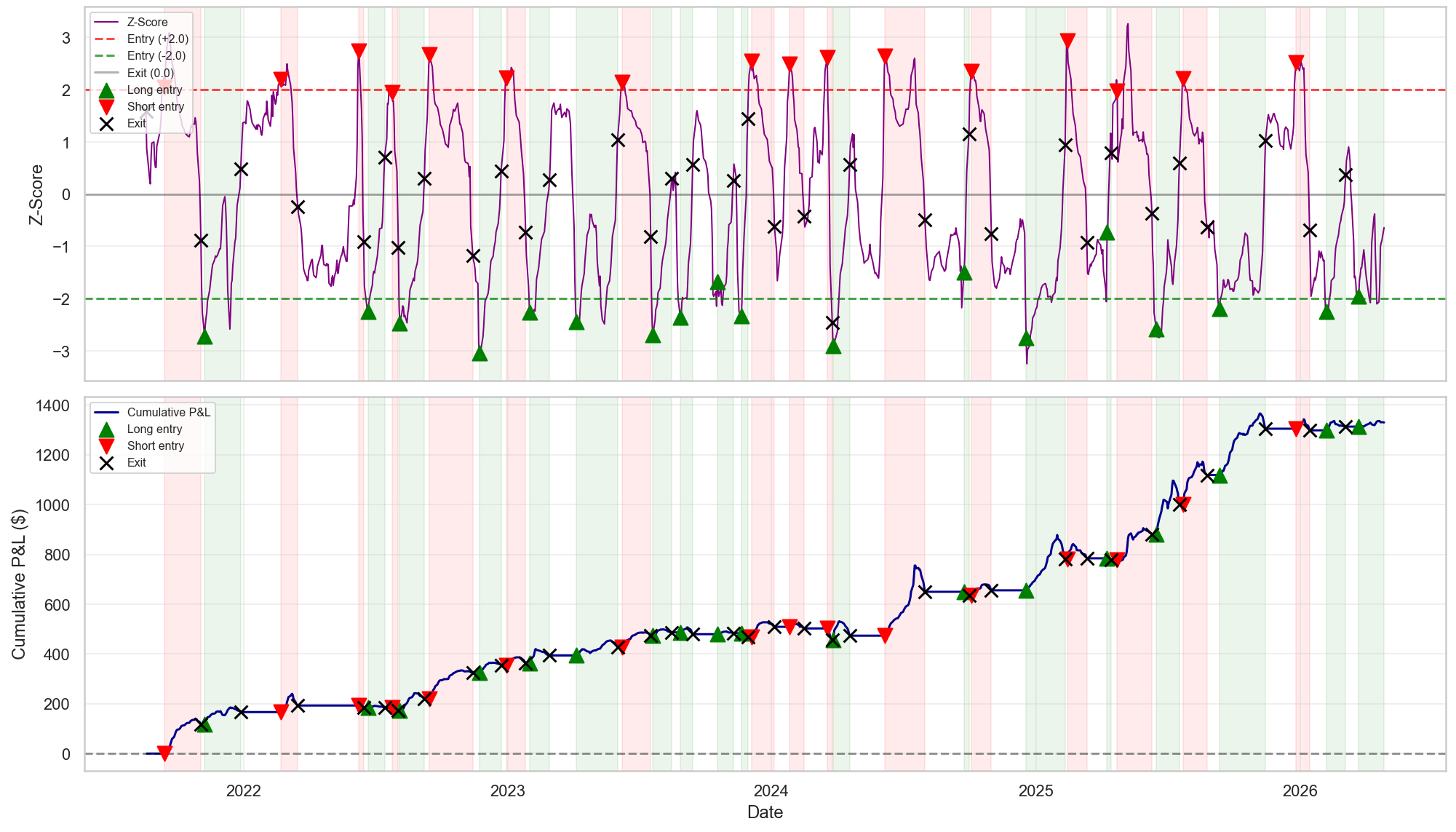

How to build a pairs trading strategy using z-score to detect mean-reverting mispricings between correlated stocks like …

Read more →

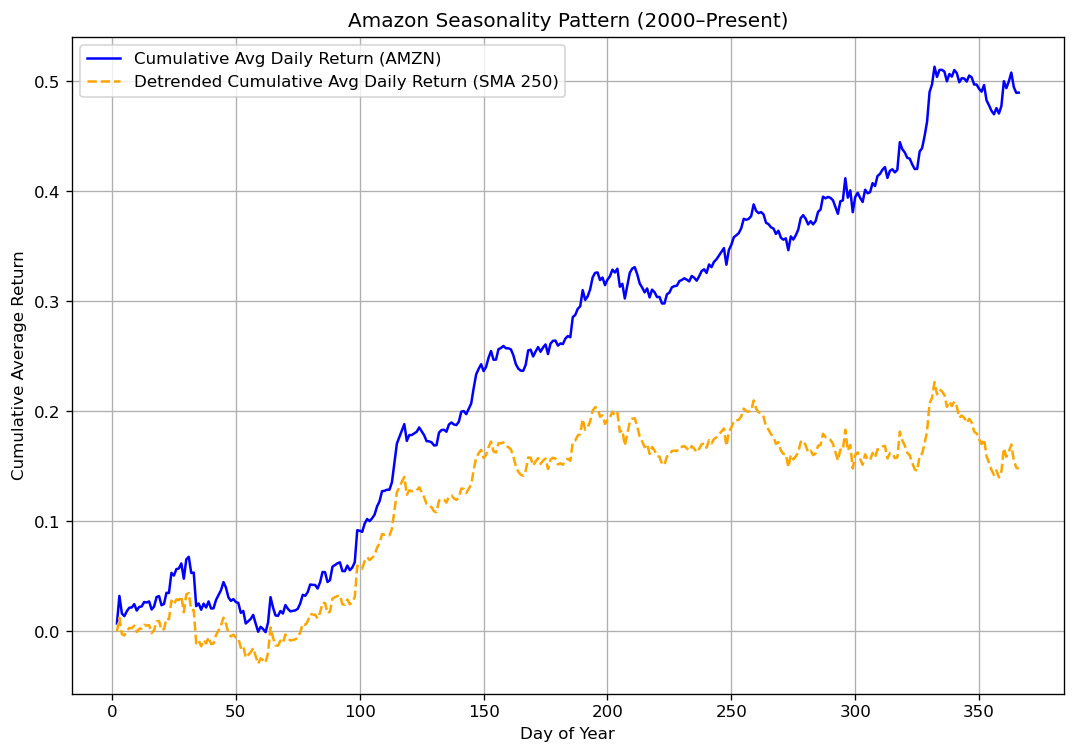

How to compute yearly cumulative returns in Python and detrend them to reveal true seasonal patterns applied to Amazon …

Read more →

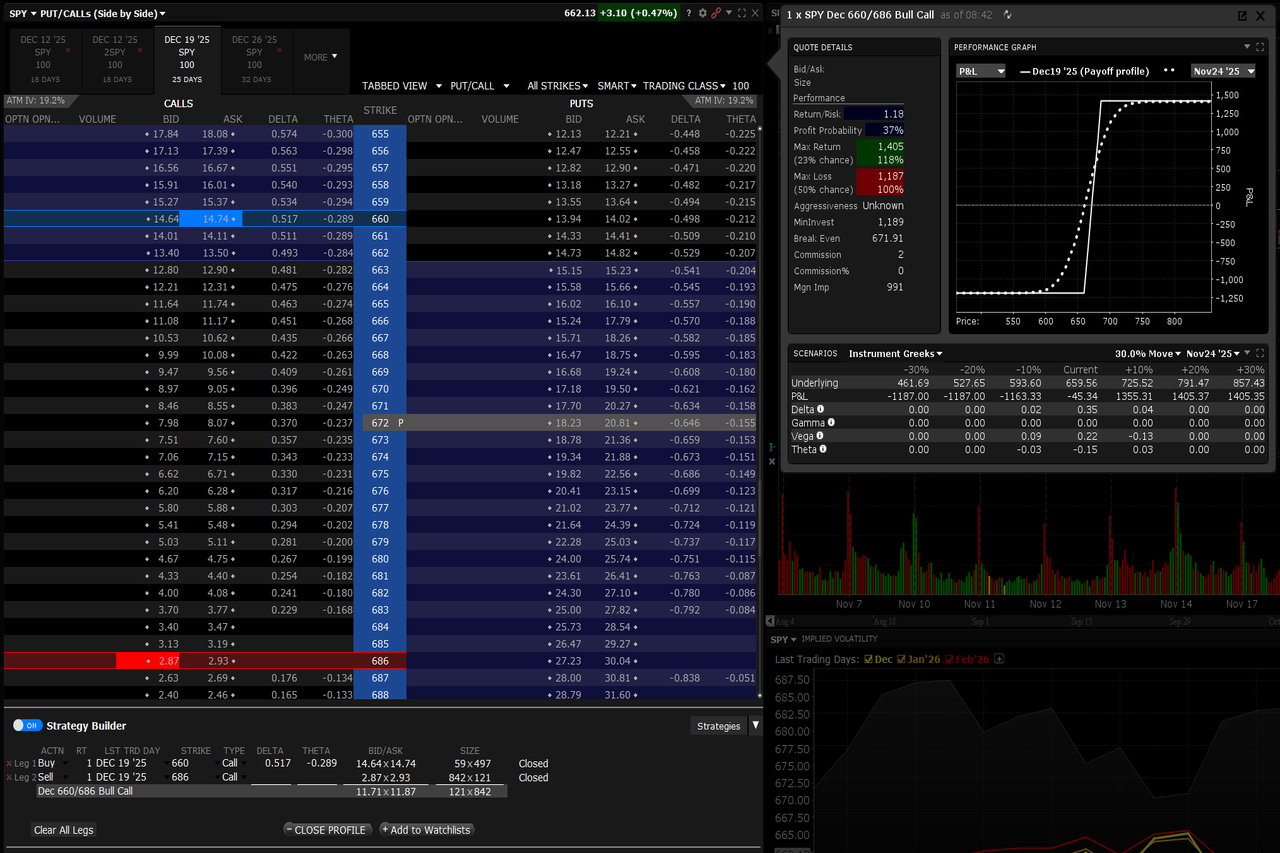

How to retrieve and analyse options chain data in Python using yfinance — expiration dates, strikes, bid/ask, Greeks and …

Read more →

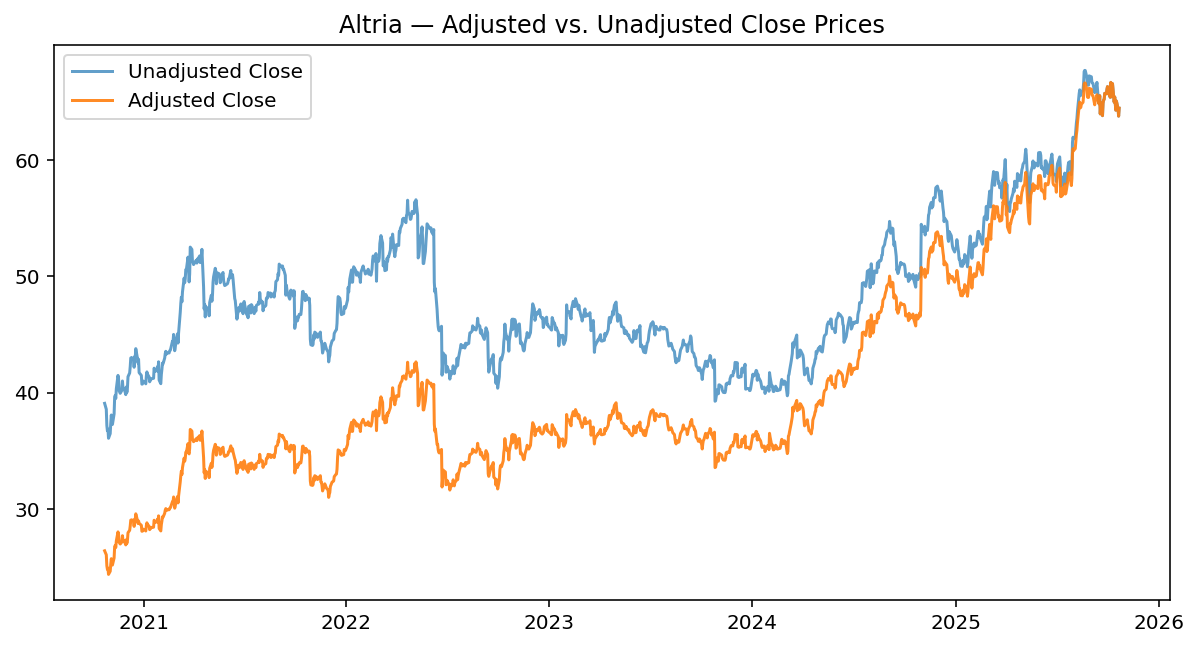

See how using unadjusted prices in a backtest silently distorts your results with a concrete Python example on Microsoft …

Read more →

Adjusted and unadjusted stock prices look similar but can make or break your backtest. Learn the difference and when to …

Read more →

How to generate walk-forward date splits in Python to properly backtest trading strategies across changing market …

Read more →

A cleaner, more reliable way to get the S&P 500 list using iShares ETF data and Python instead of scraping Wikipedia.

Read more →